Latest scientific findings show the Pacific Ocean is warming rapidly, making an El Niño event this summer highly likely – and potentially a super El Niño given the strength of the signals. Since the early 1960s, every El Niño has had a significant impact on financial markets, triggering spikes in commodity prices, higher inflation, bond market volatility, and sharp divergences in equity sector performance. But this looks like a ‘super’ El Niño, which magnifies these effects, as noted in my earlier blog.

Yet markets consistently underestimate how disruptive these events can be until the impacts are already unfolding. With a very strong El Niño expected from mid‑summer 2026 and likely to last into early 2027, the risk of a climate‑driven financial shock – layered on top of existing geopolitical and economic pressures – is rising. What might this mean for financial markets, and how can investors and market professionals mitigate the risks?

Commodities: first to be impacted

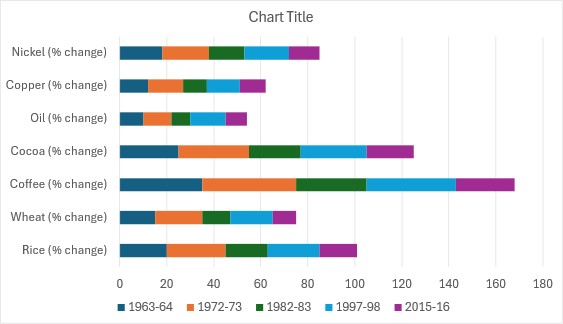

El Niño’s earliest and most visible effects appear in commodity markets. Weather instability brings drought to some regions and heavy rainfall to others. These shifts reduce crop yields and push up food prices. Rice, wheat, coffee, and cocoa all saw sharp price increases during the 1972–73, 1982–83, 1997–98, and 2015–16 events (see Chart 1).

Energy markets also feel the strain. Reduced hydropower output in some regions increases demand for oil and gas, while floods elsewhere disrupt production and transport. Metals such as copper and nickel have faced supply interruptions in Chile and Indonesia, adding volatility to industrial input prices.

In short: food, energy, and metals prices often rise sharply during El Niño episodes. These increases trigger inflation shocks that ripple into interest rates, bond markets, and equities.

Inflationary Shocks

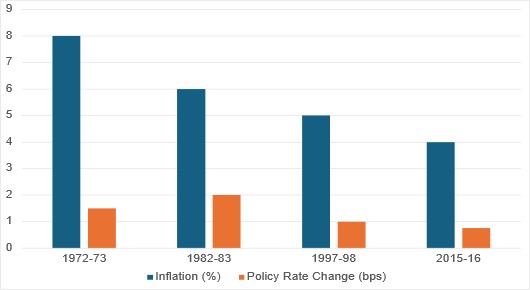

Commodity volatility feeds quickly into inflation (see Chart 2). Higher food and energy prices push up headline inflation, especially in emerging markets where food has a larger weight in consumer baskets. Historically, central banks in Asia and Africa have raised interest rates to contain food‑price inflation.

Advanced economies sometimes benefit from redirected trade flows, but inflationary pressures still spill into their bond markets. Spikes in food and energy prices have repeatedly forced central banks to tighten policy, raising bond yields and widening emerging‑market spreads.

Interest rates and Bond Market volatility

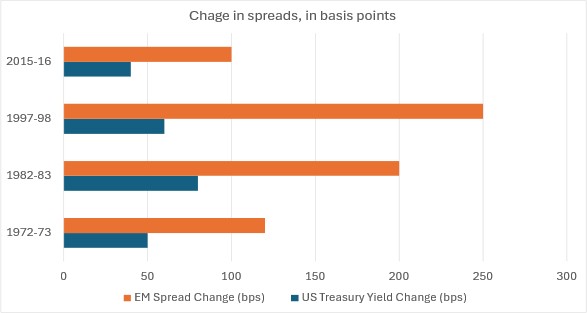

El Niño events tend to increase volatility in fixed‑income markets (see Chart 3). The Federal Reserve raised interest rates during the 1982–83 event, and Asian central banks tightened policy in 1997–98. Bond yields typically rise on inflation expectations, while emerging‑market spreads widen as investors demand higher risk premiums.

Safe‑haven flows into U.S. Treasuries and German Bunds are common. Emerging‑market debt, by contrast, often suffers capital outflows, leading to weaker currencies, higher domestic inflation, and slower growth.

The most volatile periods were 1997–98 and 1982–83. The 2015–16 El Niño also produced large swings, though somewhat muted by the post‑crisis environment of ultra‑low interest rates and large‑scale central bank asset purchases. With that backdrop unlikely to be repeated, the next event may resemble the earlier, more turbulent episodes.

Equity Sector Divergences

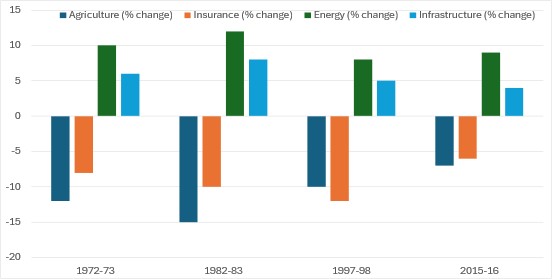

El Niño events result in divergent performance across stock market sectors. Agriculture and consumer staples typically underperform due to crop losses and increased input costs. Insurance companies encounter higher claims resulting from floods, storms, and wildfires. Conversely, energy producers often benefit from increased demand for oil and gas. Infrastructure and construction sectors may experience temporary gains from rebuilding efforts, although elevated material costs can erode profitability.

During El Niño episodes, energy producers frequently outperform, whereas the agriculture, insurance, and consumer staples sectors generally underperform (see chart 4).

Currency and Trade Effects

Currency markets also come under intense pressure. Countries that depend heavily on food imports, such as India, Pakistan, and Indonesia, feel the strain as their external trade balances worsen.

Exporters of energy or metals might see short-lived gains, but overall market volatility hurts long-term stability. Disruptions to shipping routes across the Pacific slow trade and raise freight costs, making currencies even more volatile, chiefly in emerging markets.

If these problems occur at the same time as ongoing sanctions related to the conflict in Iran and the Strait of Hormuz, then the global economy and financial system could get even worse, putting more pressure on already vulnerable countries.

Several real-time indicators are available to monitor evolving risks. Shipping rates, the Baltic Dry Index, and Drewry’s container rate benchmarks reflect stress in global freight markets. Futures prices for rice, wheat, and copper may signal impending shortages or price spikes.

Financial market impact in past El Niño cycles

- 1972–73: Food price surge contributed to global inflation and set the stage for the oil shock.

- 1982–83: Severe El Niño coincided with debt crises in Latin America, amplifying bond market stress.

- 1997–98: Commodity volatility and the Asian financial crisis overlapped, deepening equity and currency turmoil.

- 2015–16: Food and energy prices spiked, insurance claims rose, and markets began to price climate risk more seriously.

These cycles show that El Niño usually acts as a catalyst rather than as the main cause of a financial crisis. Instead, it makes existing problems worse and exposes market fault lines, causing them to fracture.

Implications for 2026/27

The next El Niño event will likely be more disruptive than past ones. Record ocean heat, higher sea levels, tighter supply chains because of recent and ongoing conflicts, and increased urbanisation could mean the financial impact is deeper and lasts longer. This is especially true for lower-income countries, which are more at risk from climate change because they lack strong infrastructure, financial resilience and insurance cover.

Southeast Asia, India, Australia, and parts of Africa have always been among the most vulnerable regions, facing big risks to crops, food security, and currency stability. Latin American exporters, especially Peru and Chile, also face major problems in farming and mining. Advanced economies like the United States and Europe will feel some effects through their supply chains, but their diverse and more resilient economies and greater access to financial resources will help them cope better.

We can expect spikes in food and energy prices; more inflation that leads to tighter monetary policy; more bond market swings, and differences in how stock sectors perform. Emerging markets are most at risk from these pressures, but advanced economies will not escape the effects.

Portfolio managers should think about hedging climate-sensitive investments early. Some practical steps include using commodity futures to lock in prices and protect against big swings in food, energy, and metals markets.

They can also rotate investments away from sectors like agriculture, insurance, or consumer staples and put more into sectors that might benefit, such as energy producers. Currency hedges are also useful, especially for portfolios with exposure to emerging markets or Asia-Pacific regions.

In addition, currency forwards and options can help protect against sudden drops in value in at-risk regions, though they do come with costs. Catastrophe bonds and weather derivatives also offer targeted protection against extreme events linked to El Niño. History shows that financial markets often adjust quickly once the El Niño’s impact is clearer and better understood or otherwise priced into expectations.

Conclusion

El Niño is expected to affect financial markets almost as much as it does the wider economy. Since 1963, every major El Niño has caused swings in commodity prices, higher inflation, changes in interest rates, and stress across multiple sectors. The risks for 2026 are potentially severe, as climate change has increased the likelihood of El Niño events. So, financial professionals should check their portfolios for any feedback loops, central banks should prepare for inflation shocks, and governments should stand ready to act as climate-driven volatility has regulatory and fiscal implications.

In response to El Niño, central banks will likely tighten monetary policy to control inflation, possibly raising interest rates and changing liquidity measures. Governments may provide targeted support, such as subsidies or relief for affected sectors like agriculture and may have to adjust trade policies to keep domestic markets stable. Working together, monetary and fiscal authorities can help reduce the economic and financial market impact of El Niño.

In summary: El Niño events leave the global economy poorer and financial markets more volatile. Recognising the pattern early – and preparing for it – is the only sure way to mitigate the shock.