Right to Buy (RTB) has changed the UK housing market more than any other policy in the past 50 years. Despite its huge impact on society, politics, inequality, and young people’s economic prospects, however, it often doesn’t get the attention it deserves.

Other big policies, like Help to Buy (which helps first-time buyers) or different types of rent controls, have made headlines but haven’t had the same lasting or widespread effects. Help to Buy enabled some people to become homeowners – mainly those who would have been able to on their own eventually –but it didn’t really change the overall balance of housing or increase the supply of affordable homes.

Rent controls have been tried or discussed in some areas, but they haven’t been used everywhere or for long. (For what it is worth, all the evidence about rent control shows that they drive up house prices and reduce the number of properties for let over time. They are not, therefore, a solution; only an increase in housing supply can reduce the cost of renting or buying a house.)

In contrast, RTB was so popular that it helped Margaret Thatcher win two landslide elections, and it still exists today with support from both Labour and Conservative governments.

This shows just how effective the RTB promotion was. People talked about there being a ‘cascade of wealth’ down the generations. Instead, it mostly benefited one generation, while future generations lost out. Many younger people now struggle to buy homes or access social housing, and we can see the social and economic effects of this today.

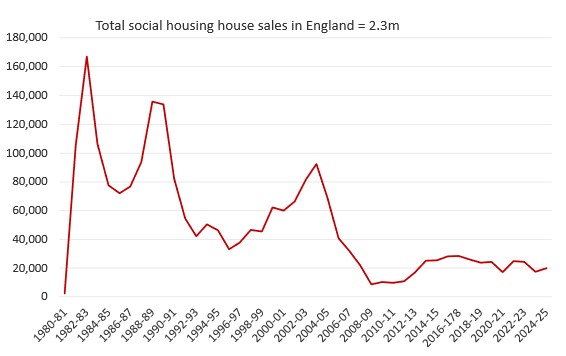

Councils were not allowed to use proceeds from home sales to build new social homes, so the number of social homes continued to decline. England, Scotland, and Wales each had their own RTB schemes, and together they sold nearly 2.4 million social homes. Most of these sales happened in England, with about 2 million homes sold.

A counterfactual – imagine no right to buy

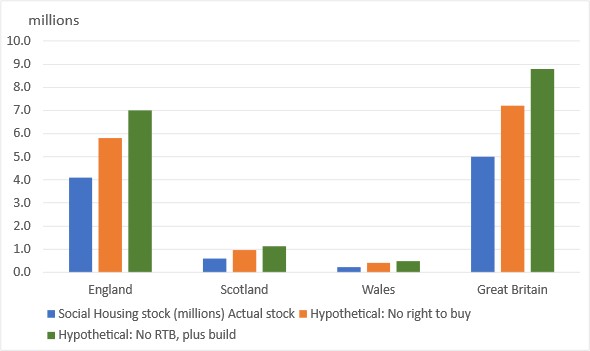

A counterfactual – suppose RTB had not happened –helps us imagine what things would be like without it. If councils had kept their housing stock and been able to build more as needed, Britain would have about five million social homes today. Without RTB, and if three-quarters of the sold homes were still around, there would be about 7.2 million social homes. That extra 2.2 million homes could have made a big difference by shortening waiting lists, reducing overcrowding, and cutting the number of families in temporary housing across the UK.

The picture becomes even more striking once we consider the collapse in social housebuilding after the early 1980s. Before RTB, Britain regularly built lots of social housing. Councils and housing associations added tens of thousands of homes each year, which helped keep rents lower overall. If social landlords had kept building just 40,000 extra homes a year, over forty years, there would be about 1.6 million more social homes today. More Britons would live in secure, low‑rent accommodation. The private rented sector would be smaller, less dominant and less expensive.

The owner‑occupied sector would still be the majority tenure, but it would be operating in a market with far less scarcity at the lower end. The consequences would be felt across prices, rents, household finances, labour mobility and the distribution of wealth.

The winners and losers from Right to Buy

Another important point is who gained and who lost from RTB. Council homes were built with money from all taxpayers, so everyone helped pay for them. But the financial benefits mostly went to a small group – people who were council tenants at the right time and could afford to buy. Most buyers were older, long-term tenants, often with steady jobs and usually white British. Surveys show that families and older couples bought more often, while single people and minority groups were less likely to benefit.

The pattern across regions was also uneven. London and the Southeast saw the most homes sold, with some inner London areas selling more than half their council houses to private owners. In contrast, sales were significantly lower in the Northeast, Scotland and Wales. This meant that problems like longer waiting lists, higher private rents and more people needing temporary housing were worst in busy cities where the demand was highest.

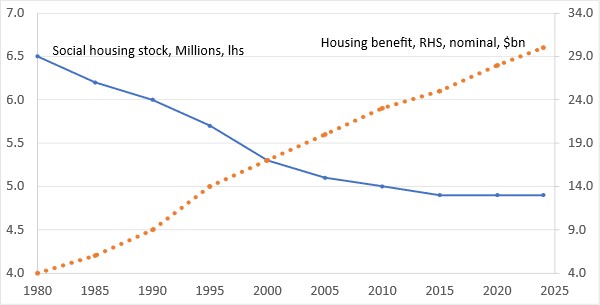

This brings up a basic fairness question: who paid, who benefited, and who missed out? From a tax perspective, the policy shifted public housing assets to a small group. Meanwhile, the long-term costs – such as higher rents, greater spending on housing benefits, and fewer affordable homes – have been felt by everyone, as charts 3 and 4 show.

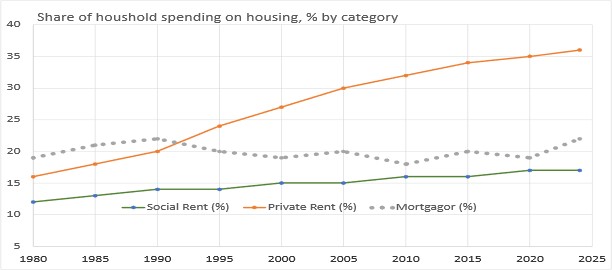

This unequal distribution of gains is reflected in the long‑run shift in housing tenure. Over the past four decades, social renting has declined sharply while private renting has more than doubled, with owner‑occupation peaking in the early 2000s before falling back.

Chart 4 illustrates this structural transformation: the UK has moved from a balanced tenure system to one dominated by higher‑cost private renting. This shift underpins many of the pressures now seen in affordability, inequality and household financial fragility.

Addressing the disparities created by RTB

Going forward, future social housing policy could address these disparities using targeted measures such as regional delivery targets aligned with areas that experienced the greatest stock loss and now face the highest housing pressures. To operationalise this, the government could implement a statutory regional allocation formula, requiring the Homes England funding framework to set minimum proportions of new social housing to be delivered in high-need local authorities based on regularly updated metrics of need and historic dispossession.

Legislation could mandate periodic reviews of allocation data, overseen by an independent regulator, to ensure fairness and transparency and enable corrective adjustments. Funding streams should support inclusive, accessible, and mixed-tenure developments in both urban and rural areas, potentially through earmarked grants tied to explicit inclusion targets. This could include specific ringfenced funds for accessible housing modifications, as well as incentives that reward councils for meeting diversity and regional equity benchmarks.

Making equity an explicit goal in the scale, location and allocation of new social housing would ensure that future investment is more distributed. If fairness is made a clear goal when deciding how much and where to build new social housing, future investment would be more evenly spread than under RTB.

The GDP cost of the housing crisis

Recent research for Homes England shows that high housing costs now cut UK GDP by 1–2 per cent each year, mainly because people can’t move easily for work and companies must pay higher wages in expensive areas. This estimate is based on comparing regions with different housing costs, using models that account for factors such as jobs, migration and wage differences. The research suggests that if housing were more affordable, people could move more freely for work, helping the economy run better. Right now, this loss is about £23–£46 billion a year – the same as losing all the economic output of a city like Bristol or Nottingham.

This happens because workers can’t move to better jobs, companies pay more to attract staff, and families spend more on housing instead of other things. It also means they spend less time on additional courses and skills training because most of their time is spent working to pay ongoing bills, leaving little time to look ahead and upskill. It shows that the housing shortage is not just a social problem, but a real drag on the UK economy.

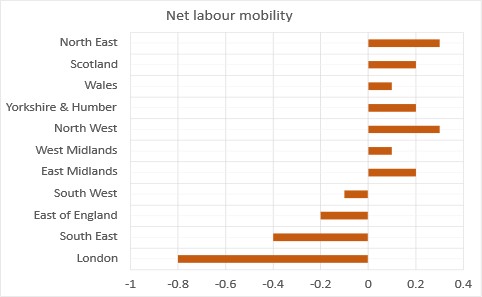

Chart 5 shows the clear divide between high‑cost and lower‑cost regions in terms of labour mobility. London and the Southeast are experiencing sustained net outflows of working‑age people, reflecting the pressure of high housing costs and limited affordability. In contrast, regions with lower price‑to‑income ratios – such as the Northwest, Northeast, Scotland and Yorkshire & Humber – are seeing modest net inflows.

This pattern highlights a structural misallocation problem: workers are moving away from the most productive, opportunity‑rich areas because they cannot afford to live there, dampening both regional growth and national productivity.

High housing costs have slowed down productivity. When workers can’t afford to move to places with more jobs, the economy misses out on matching people to the right work. Companies also face problems, since they must pay higher wages in expensive areas, which increases their costs and makes them less competitive.

Sometimes, businesses don’t expand in these areas at all because the cost of hiring staff is too high. This means both workers and money aren’t used as well as they could be, and productivity grows more slowly than it would if housing were more affordable. This relationship is visible when comparing regional affordability with labour mobility.

The price‑to‑income ratio chart shows the stark affordability gradient across the UK. London and the Southeast sit at the top end, with house prices far outpacing local earnings, while regions such as the Northeast, Scotland and Wales remain significantly more affordable.

The income hit to households

It’s also important to look at the bigger economic picture. High housing costs slow down spending, leaves people with less money, and make the economy riskier. If there were more social housing, it would help keep housing costs steady and make households more secure. The financial system would be less affected by ups and downs in the housing market, and the economy wouldn’t rely so much on rising house prices to keep people spending.

The data also shows that while homeownership policies are popular because they help families build wealth and feel secure, the way these benefits were shared has led to big social and economic problems. Instead of making the economy stronger or society richer, the long-term result has been more financial insecurity and greater social division in Britain.

Losing millions of low-rent homes has left more people exposed to high market rents, pushed up the cost of living, and widened wealth and regional gaps. Wanting to own a home is understandable, but the main problem is that the benefits of building wealth through property have gone to a small group, while most people now have less access to secure, affordable housing.

The counterfactual shows a larger social housing stock. Looking at what could have happened, having more social housing would have helped keep the economy steady, made wealth more equal, and slowed down house price rises. Instead, we now have a system in which housing takes up a larger share of people’s income, wealth gaps have widened by happenstance, and lower-income families bear the brunt of housing market ups and downs.

How much new social housing do we need to fix this?

Three options stand out. A national target to deliver 90,000 to 100,000 new social rent homes per year for at least a decade would begin to reverse the long-term deficit. Reforms to land policy, such as enabling local authorities to acquire land at existing use value and streamlining planning for public-led developments, would help unlock sites and reduce costs. Removing borrowing caps on council housing investment and expanding grant funding through schemes like the Affordable Homes Programme (AHP) would enable councils and housing associations to scale up delivery.

But reaching this level of building won’t be easy. Political changes and local opposition can slow things down or stop them altogether. Money is also a problem, since public budgets are tight and building costs are rising. Complicated planning rules and long approval times often delay projects, especially where people object to new social housing or where roads and services aren’t ready. There are also worker shortages, and building materials are more expensive, making it even harder to build new homes quickly.

On the other hand, if all political parties agreed on the need for affordable housing, it would be easier to maintain investments and policies over time. New ideas, such as adopting modern building methods or making it easier for councils to buy services, could speed up construction and keep costs down. Working together – councils, housing associations, private companies, and community groups – can bring in more skills and money. Getting the public on board with clear communication can also help. Finally, funding needs to be flexible, reliable, and able to keep up with rising costs to turn these plans into real homes.

Looking at both the challenges and the things that can help unlock more building is key to understanding how realistic and urgent new social housing policies are.

Setting aside money from RTB sales to reinvest in new and existing social housing would help maintain the number of homes. Improving current homes to be more energy-efficient and accessible would ensure the sector meets the needs of all household types. These steps together would help build a fairer and stronger housing system.

The long-run consequences are with us today

Looking at what might have happened shows the long-term economic and social effects of RTB. The policy significantly reduced the social housing sector. It shifted the balance toward private housing, which is increasingly difficult for those on average incomes, especially as those incomes have stagnated in real terms since the 2008/9 global financial crisis.

As a result, the housing market is more expensive, less stable, and less equal than it would have been. We can see this in higher house prices compared to incomes, more people renting privately, higher spending on housing benefits, and more pressure on local councils. Today, there are about five million social homes. Without RTB, there would be about 7.2 million. If building had continued at a steady pace, there could be nearly 8.8 million. The difference – almost four million homes – is the main reason for many of the problems in today’s UK housing market, with negative wider societal and economic effects.

Conclusion

Looking at what could have happened helps us see what’s wrong with the UK’s housing market and how to fix it. The market we have now is the result of choices made decades ago. Today, over 1.2 million households are waiting for social housing in England, Scotland, and Wales – a backlog caused by selling off social homes and not building enough for more than 40 years.

The RTB policy and the drop in social housebuilding continue to affect prices, rents, inequality, and poverty to this day. But there are ways to improve things. The most important step is to start a bold, long-term plan to build enough social housing to meet the need and make the system fairer, more secure, and more affordable for everyone.

The result would be faster economic growth driven by productivity gains, making it more sustainable and durable. With an ageing population, fewer people are paying into the tax system as the working-age population shrinks, and more are taking out as the number of retirees rises, so there is an urgent need to boost productivity.