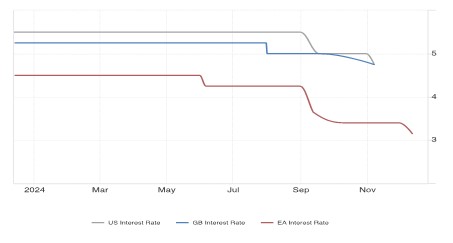

Financial markets are betting this week that the Bank of England will not cut its key interest rates but leave them on hold at 4.75%. The market consensus from Trading Economics is that the 9-strong committee on Thursday, the 19th, will vote 8:1 to leave the UK Bank rate at 4.75%. That is despite annual UK consumer price inflation of 2.3% in October – though it is expected to rise to between 2.4% and 2.6% in the year to November.

That view of the UK is in stark contrast to expectations that the US central bank is expected to cut its key rate by a quarter of a point to 4.5% at their meeting on Wednesday. The European Central Bank (ECB), at its meeting last week, cut interest rates to 3%, as shown in chart 1.

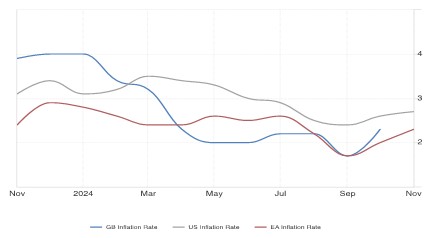

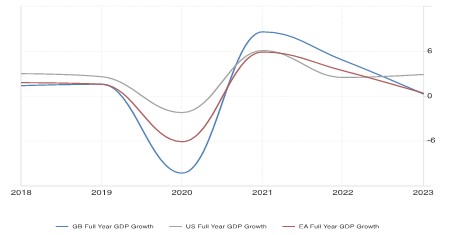

Euro area economic growth was just 0.4% in the year to September, and its annual inflation rate was 2.3% in the year to October. Yet it cut interest rates for the third consecutive time this year to 3%. US annual consumer price inflation was 2.7% in the year to October, see chart 2, and its central bank is still expected to cut interest rates despite a yearly GDP growth rate of 2.8%, see chart 3.

The European economic and inflation performance is closer to the UK’s than the US. Therefore, the Bank of England’s reluctance shows that it is far more cautious than the European or US central banks regarding price inflation, given its growth rate is on par with that of the EU as is its inflation rate as the relevant charts attest. The difference must come down to the mindset of the Monetary Policy Committee (MPC) itself and its philosophy about the ‘stickiness’ of inflation, which refers to the tendency of price inflation to remain at a high level despite changes in economic conditions.

Bank watchers also speculate about the MPC’s strategy, particularly its wait-and-see approach to the effects of the new government’s Budget, which the Office for Budget Responsibility (OBR) predicts will be negative in the short term. MPC members also seem focused on the potential impact of services price inflation and wage-price inflation rather than on the general trend of economic growth and overall price inflation.

Other central banks have cut rates even more aggressively in the past week than France. The Swiss National Bank, for instance, cut interest rates from 1% to 0.5%, and the Bank of Canada cut its key policy rate by half a percentage point to 3.25%, the fifth cut in a row. If the US were to cut, it would be ignoring the potential effect of an incoming administration that is widely expected to cut taxes and, therefore, give the US economy even more of a boost in 2025. Despite the caveats, the Bank of England could surprise on Thursday by cutting interest rates by 0.25%, aligning with the US’s expected move and giving everyone an early Christmas present.