One of the oddities about the narrative on the direction of interest rates is the argument that, because consumer price inflation is still above the 2% target, the Bank of England cannot cut interest rates. That suggests that interest rate policy changes immediately impact the current inflation rate in the short term. However, this view must be challenged, as analysis of the link between policy changes and inflation shows that this is simply not the case.

The impact on inflation of a change in interest rates acts with a lag of up to two years. In other words, changing interest rates today will not have the maximum impact on inflation as much as 18 months later. It means that even if inflation has yet to fall to its target, monetary policy must act early to prevent it from falling significantly below the target in future. The longer the wait before relaxing policy, the further below the target inflation will eventually reach.

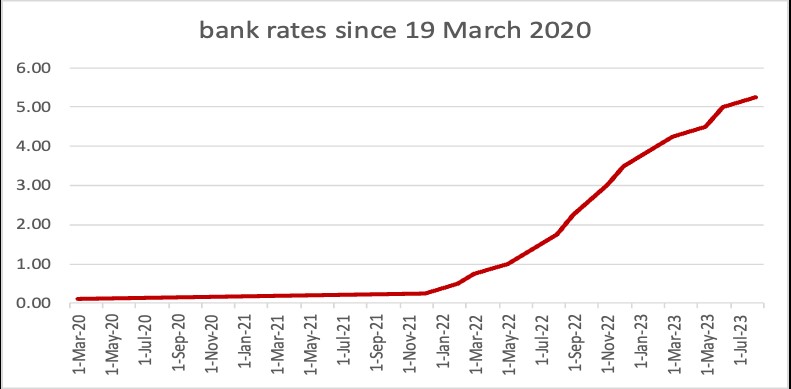

One could argue that we are at one of those inflexion points now. Although the current inflation rate is 4%, some factors leading to its fall have yet to be fully reflected in the data. One of these factors is the 14 interest rate increases since 2021, see chart 1.

Understanding inflationary pressures

However, the increases seen in interest rates are only one of the factors leading to the fall in price inflation – and currently the least important. The decline in energy and food prices is far more critical to the drop in price inflation. That’s happening because of the unwinding of the supply-side inflation shock caused two years ago by Russia’s invasion of Ukraine, which helped drive the initial spike in inflation. Falls in global food prices have yet to be fully seen in the UK, however.

Another reason price inflation is falling and will likely fall further is because money supply growth in the UK is contracting and, therefore, no longer adding to inflation pressure in the UK. That means that policymakers must consider the energy price effect, the unwinding of the supply side shock from the war, the fall in monetary supply, and the consequences of its earlier tightening of interest rates when judging where inflation will be over its two-year forecast horizon.

A call to act

Considering those factors and the dropping into recession in the second half of last year, interest rates should be cut immediately, unlikely though that may be. These factors are why there is pressure on the Bank of England to cut rates at the next quarterly meeting, which is held in May. That said, there’s a clear case for not waiting until May but acting at the March meeting, Budget on the 6th notwithstanding.

The evidence from the GDP figures is that the UK economy is in recession and unlikely to recover significantly anytime soon. Therefore, cutting interest rates now would help prevent the unnecessary slow growth that is likely, and prevent inflation from falling well below the 2% two-year medium-term target.

Wages are not fuelling inflation

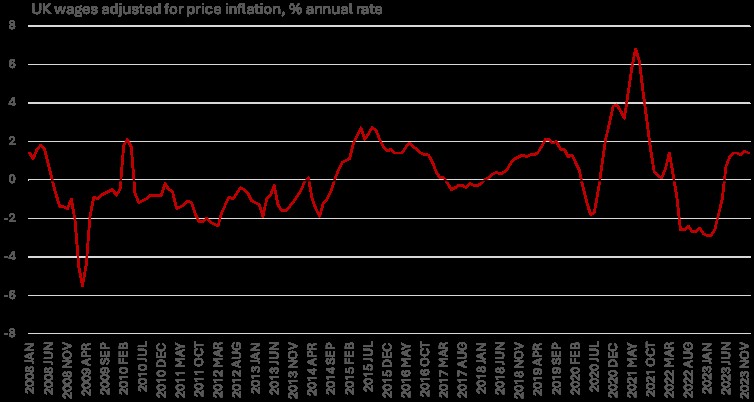

Another shibboleth worth challenging is that wage inflation is a barrier to lower price inflation and, therefore, to lower interest rates. Adjusted for price inflation, wages are barely higher than in 2008, so it’s not responsible for the high consumer price inflation rate. Nor has price inflation driven up wages – which are currently falling back. The reason is that firms pay salaries out of corporate earnings, determined by their ability to efficiently sell goods or services provided to the public.

Successful firms have wider profit margins, allowing them to pay workers more and reflect their contribution to those profits. But not-so-successful firms will go bust if they follow suit, meaning higher unemployment, as their productivity cannot sustain a cost structure that pays workers more than their productivity.

So, high wage inflation does not automatically mean higher price inflation. Raising labour productivity by buying new machinery or upskilling staff and increasing profit margins can boost pay. However, this is not inflationary, as it’s made by producing more output per unit input.

With a slow-growing economy, profit margins under pressure, and poor productivity, firms can only pay workers what is justified by their ability to grow profits. Therefore, the supposed link between wage and price inflation is neither correct in theory nor practice.

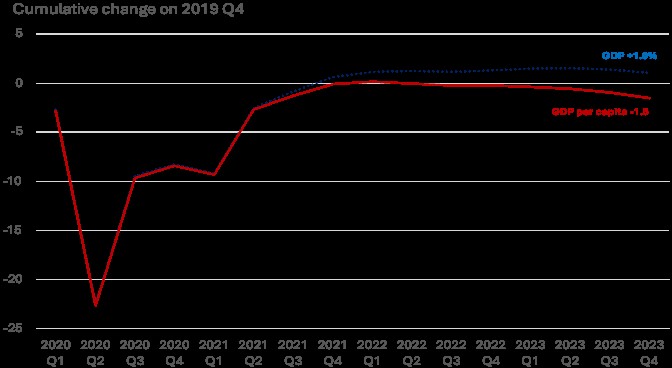

Chart 3 shows that cumulative quarterly GDP has poorly performed compared to its level since the 2020 drop – especially in terms of GDP per capita where there has been a fall of 1.5%. After a quarterly pickup following the 2020 lockdown, the economy has returned to negative growth, with GDP down 0.3% in Q4 2024 after sliding 0.1% in Q3. The Bank of England forecasts GDP growth this year will be ¾% (after just 0.1% last year on the latest estimates). The forecast for 2025 is growth of 1%. These are not inflationary growth rates and suggest inflation will be under little upward pressure from the pace of domestic demand growth any time soon. Yet it’s such a concern of a rebound in growth that one member of the MPC cited for voting for a rate rise at the last MPC meeting.

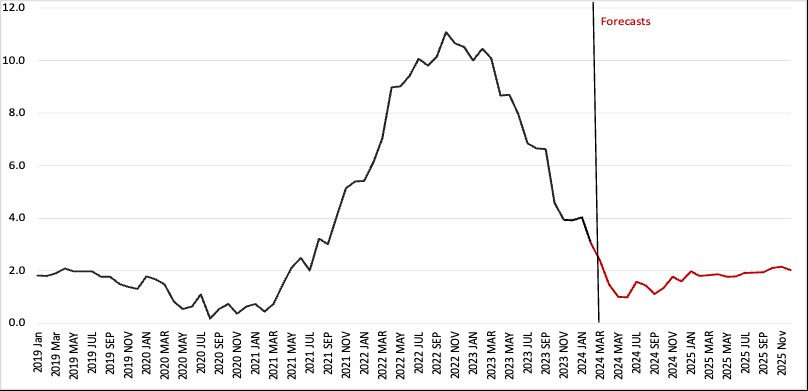

We reflect that weakness in our forecast of the annual inflation rate, which we expect to be well below 2% in April, see chart. It will stay below the 2% target for the rest of this year and only rise to 2% towards the end of 2025.

Rate cuts to support recovery

In this scenario, financial markets and policymakers will likely revise price inflation and interest rate projections lower in the year ahead. That is not to say that UK economic growth will not rebound. The monthly data flow of purchasing managers’ indices (PMI) for services and manufacturing suggests that Q1 2024 may see a return to modest expansion. But that should not prevent rate cuts, as the economic rebound will be from recession to stagnation and not lead to demand led inflation.