With inflation falling sharply in the US, the eurozone, and the UK, there is no longer a debate about whether the peak in interest rates has been reached. Instead, there is a consensus about rate cuts being the next move, not rate rises and about when that will happen, not if.

Financial markets are now ‘pricing in’ interest rate cuts in these countries during 2024 – a reversal of their expectations a few short months ago when they were still expecting further rate hikes.

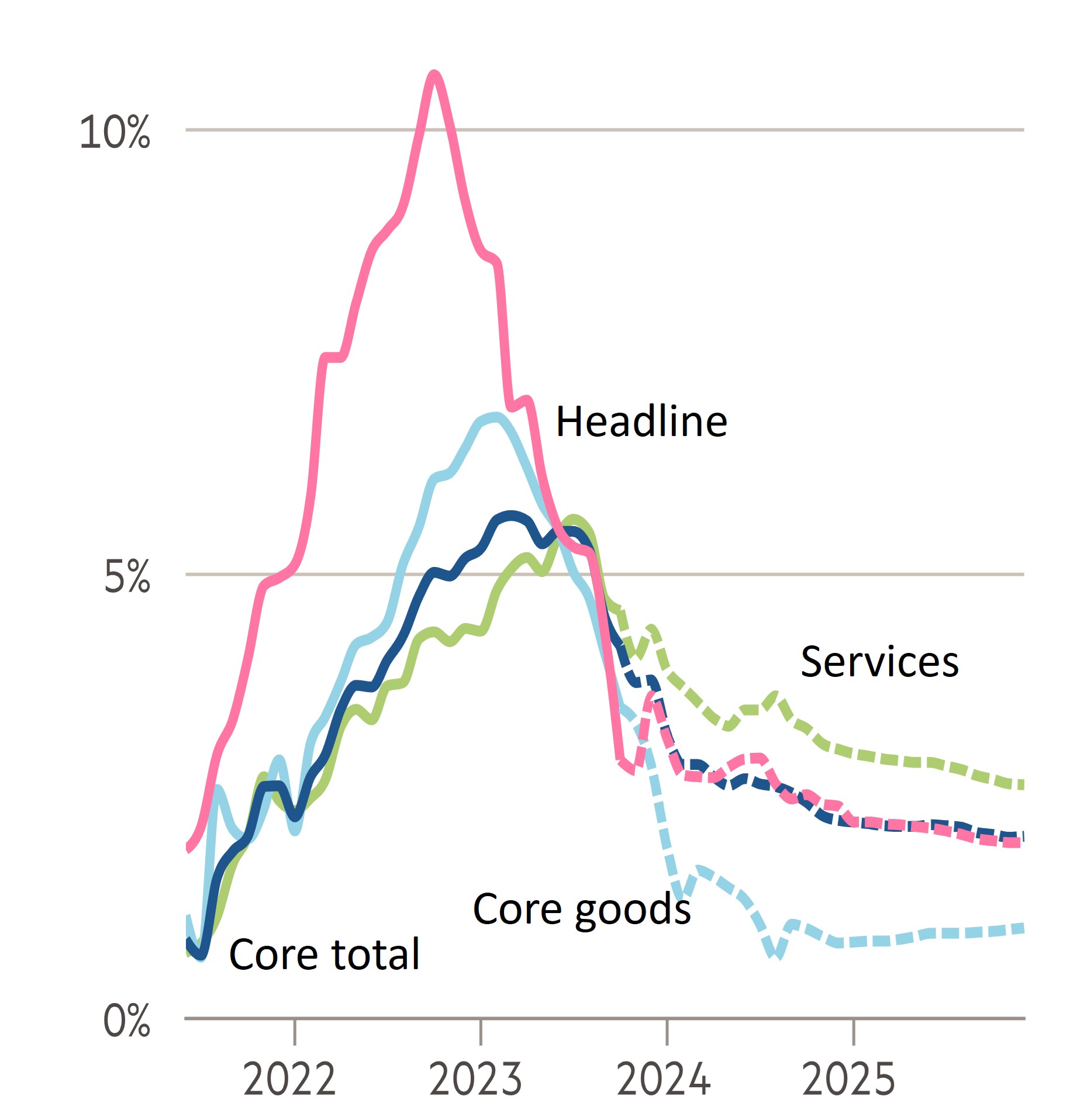

Although seasonal food and energy prices remain elevated in measures of consumer price inflation, headline CPI rates for October have dropped to 3.2% in the US, 2.9% in the eurozone, and 4.6% in the UK; they are significantly off their highs.

The declines in price inflation illustrate the unwinding of the supply-side shock of Russia’s invasion of Ukraine, which pushed up energy and food prices from February 2022 onwards and some of which is falling of annual indices, and the impact of a subsequent tighter monetary policy stance on the pace of economic activity.

A reversal of quantitative easing by selling bonds accumulated since the Global Finance Crisis (GFC) is compounding the negative impact of higher interest rates on economic growth by contributing to a fall in broad money supply, as shown in chart 3.

That could lead to even weaker economic growth than we’re seeing now, particularly in the US, where it’s still buoyant compared with the EU, see chart 4. The combination of contracting money and weak economic growth will push down price inflation in the US and EU towards targeted levels or under by the end of 2024.

Focus on the UK

Although the UK’s inflation rate is currently higher than that of the eurozone or the US, it faces a greater risk of price deflation because its broad money supply is contracting more sharply than the US and Eurozone. A worse productivity performance than in the US or the eurozone will further weaken the UK economy and push consumer price inflation towards negative territory in 2025 or 2026.

Price inflation expectations should now move significantly lower if, as expected, economic growth remains in the doldrums. So, it’s a picture of an economy that should see some reasonably sharp interest rate cuts in 2024. As Chart 6 shows, financial markets are already pricing in this trend. Rate cuts are expected in May, September, and the final quarter of next year based on market data produced by the Bank of England and shown in the chart.

With around 50% of the effects of higher interest rates yet to impact the economy, the risk is price deflation and an economy that could experience recession whether it is hit by any further adverse shocks or not.

In this environment, it would be astonishing if consumer inflation did not hit the 2% target before the end of 2024. If not that year, we must expect it in early 2025. Given the lags in monetary policy, significant monetary loosening will be required sooner rather than later to prevent consumer price inflation from falling below the 2% target.

However, that will be too radical a series of cuts to expect of the monetary authorities at this stage of the economic cycle and without further evidence of inflation falling below target and of economic contraction. Hence, the risk is that the economy continues to skirt recession, and inflation will fall below a 2% annual increase and possibly into deflation territory in 2025.

Paradoxically, it could have a positive political effect on the incumbent government because interest rates will be falling in an election year. That should be of some assistance to the electoral chances of the incumbent political party as it chooses a date to hold the General Election in 2024.

But that said, the reality is that the UK economy will register little or no growth and remain fragile, unemployment will push further above 4%, and company and mortgage defaults will still rise through 2024. A snap election, anyone?