It seems churlish to say that this was a Budget packed with detail but no overarching strategic vision or plan. It was, after all, billed as a Budget for a seminal moment in the UK. It was coming at the end of the first global pandemic since 1918, and it was the first one in a post-Brexit environment. Hence, one would have thought that it would have commented both about the future of Britain post-Covid-19 and outside of the economic union. Sadly, there’s very little of either in a strategic view of where the UK is heading, how it will get there and what it will do or be once there.

Firstly, what was in the Budget and then what was missing? Or, in my view, what are its fatal flaws?

It was a Budget that played to both the argument for supporting the economy until recovery took hold and for reining in the public finances over the longer term. It was a ‘support the economy now, pay for it later’ approach that most support, whilst at the same time, sticking to the Conservative credo of market liberalism and small government.

It has to be said that this was no Budget for a Thatcherite or post-Thatcherite Britain. There was no bonfire of regulations, no axe to business taxes that ‘hold back growth’ now that the UK is in a post-Brexit world, free of the shackles of a ‘sclerotic’ Europe. In short, no free market opening to the world and no ‘Singapore’ on the Thames.

The Budget can be summarised in the three charts depicted. One shows that GDP grows strongly this year and then slows back to around 1½% a year, while consumer price inflation remains well below target. So, no transformation in the UK’s long-term growth prospects there. But crucially, low inflation allows for interest rates to be only modestly higher at the end of the forecast period.

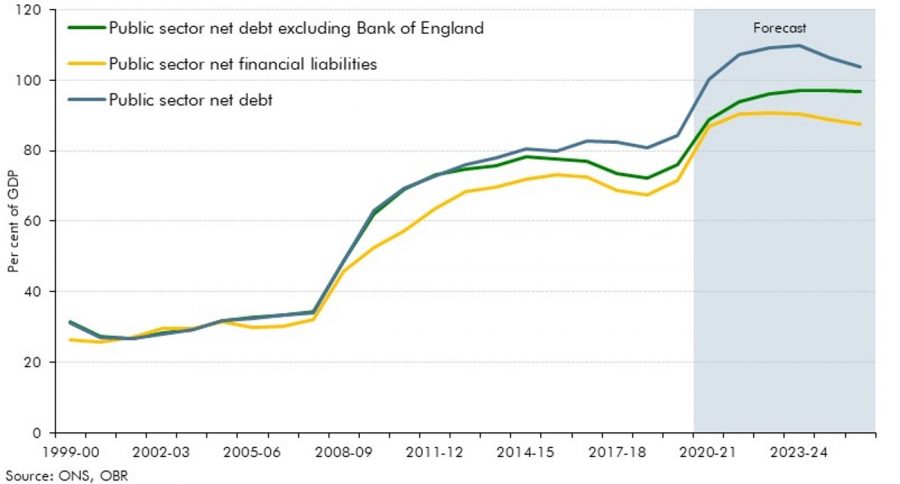

The second chart shows that outstanding UK debt rises to over 100% of GDP and remains that way over the period to 2025 – in other words, for the longer term. What will be crucial in keeping down interest payments on the high level of debt is low interest rates, beget by low inflation. The OBR has estimated that for every 1 percentage point rise in long-term interest rates above their assumption, the debt level will rise by £20.4bn. So, a 5-percentage point rise would add over £100bn.

The third chart shows that tax as a share of GDP rises to the highest level since the 1960s and will certainly be above the low it reached in the late 1980s. This means that this is not a Budget that has curbed the increase in the public sector’s GDP share, nor is it one that has meaningfully cut business taxes in a dash for growth through greater productivity gains.

However, there are tax increases on individuals, through the freezing of tax allowances, and on companies, through a rise in the Corporation tax rate from 19% to 25% in 2023. There is also freezing of departmental spending, which effectively means cuts in spending on non-ring-fenced services, around 15%. Yet debt still rises, showing the extent of upward pressure on public spending. This is, to reiterate, not a tax-cutting drive for growth Budget but one that does a bit to tighten the fiscal stance, a sort of mini austerity.

This is an issue for many that bringing order to the public finances is not being done through faster growth, thus bringing down the overall debt to GDP ratio – but instead by raising taxes and cuts in spending. But these two latter actions seem inadequate to the task. Perhaps this incompatibility is why there were no medium-term fiscal rules in the Budget – they would be broken – simply one to bring down the debt to GDP ratio from this year’s level.

So, the question is: are the Budget numbers possible, given the UK’s economic and public spending realities in the coming years? For instance, since the Pandemic, 1.3 million people have left the UK, creating the risk of slower growth and less tax revenue if they do not return.

Take another example, tax allowances. When it was introduced, it was meant to represent one years’ salary on the minimum wage. On that basis, it should currently be £17,374.50p based on a minimum wage of £8.91 and a working week of 37.5 hours rather than what it is, £12,500 a year. Freezing this until 2026 will mean over a million low paid workers will start to pay taxes, exacerbating in-work poverty.

This leads us to what was not said in the Budget.

The UK has a productivity problem, which is what holds back economic growth. It has the lowest productivity compared with the other G7 economies. Since the financial crisis of 2007/08, UK productivity growth has been roughly flat year on year. That means economic growth is essentially coming from an expansion in the workforce. So, will 1.3 million fewer people make no difference?

Office for Budget Responsibility (OBR) figures show that there was a fall of 1.3m. Little said about how to rectify this and the capital allowance change, which will only last for three years to replace the higher corporate tax, is unlikely to lead to a productivity boom. At the same time, nothing was said about Brexit in the Budget.

But the OBR’s statistics show that Brexit will take 4% off the UK’s long-term growth rate. It loses access to workers at affordable rates and in a timely manner for UK companies. It makes it more difficult for it to export seamlessly into a large market which would help UK companies to grow and be more competitive and productive. Nothing was explicitly said about these issues and others, like those affecting UK services exports or Northern Ireland.

The UK faces upward pressure on all of its public services from an ageing population. One key aspect of this is the pressure on care homes, reflecting both the ageing population and the higher cost of looking after them. The UK also has a housing crisis, with not enough homes being built for those who cannot afford to buy. This will remain the case and be exacerbated by the scheme to underwrite 5% of mortgages for those who can afford to buy a home anyway, with little said or done about those who cannot afford to buy.

That the UK needs at least 300,000 homes to be built per annum was not mentioned, nor that it is doing only half of that figure today. Hence, the right to rent sector was once again neglected and will result in a deepening of the social housing crisis. It is not recognised that many people cannot afford to buy and must rent from social landlords.

The lack of mention of these issues says a lot about the UK authorities’ lack of vision in the context of an obviously ageing population, of low productivity, of the post Brexit environment and the challenge posed by the inevitable faster pace of technology which is leading to significant changes in society.

Are we really to believe that the biggest health crisis in 100 years, which has killed 125,000 people so far, exposed the frailties, inequalities, and faultiness in our society, will not lead to some profound changes? I think it will and should not be ignored. Withdrawing safety nets to vulnerable groups – taking the example of those most exposed to the virus – those so-called essential workers. Will they be allowed to fall behind in living standards and to have poor working conditions? This seems politically untenable.

Just after the First World War (and flu pandemic which killed about 100 million worldwide), a new UK social contract was forged. The age of deference was over. There was another after the Second World War and yet another after the upheavals and great inflation of the 1970s. With Thatcher’s advent, this latter social contract focused on opening up an over unionised UK economy to the world (including the EU single market) and adopting best global practices in production, management, technology, and financial markets.

This era came to an end with the financial crisis of 2007/08. But nothing has replaced it. Now, the pandemic will force further social pressure for change. This Budget addresses none of these issues.

A future in which the pace of technology is accelerating – leaving many people behind as there will be a skills mismatch in the fast growth phase – an ageing population, and with the UK having left the world’s biggest trading block after 50 years of membership will be challenging. All this argues for an adventurous budget for our times, charting a future course through all of these challenges and opportunities. This lack of vision, scale and breadth are why I would not commend this Budget; however, I would accept the sentiment in the quote from Alfred Tennyson’s poem used in it: ‘that which we are, we are’ but perhaps not quite how the Chancellor meant it. It’s worth quoting the whole segment: ‘and if we are ever to be any better, now is the time to begin’. Now, I would certainly agree with the last sentiment.