Last week delivered something the private-credit industry has largely avoided for more than a decade: a genuine, system-wide liquidity test. More than $20bn in redemption requests hit the largest managers — Apollo, Ares, Blackstone, Barings, Cliffwater, Morgan Stanley and Blue Owl. That was the first time that an asset class that has grown into a $1.8 trillion force in modern finance, has experienced a significant setback. The core of this stress is a fundamental contradiction: private credit funds offer investors periodic liquidity— often quarterly — while the underlying assets—customised, privately negotiated loans—are inherently illiquid.

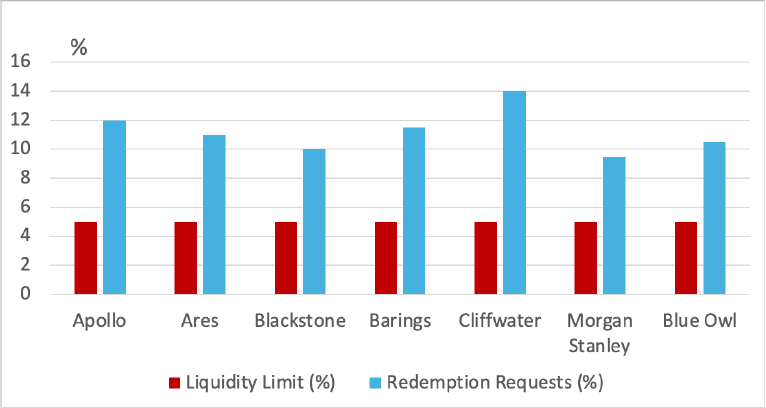

These loans are designed to be held until maturity rather than traded. This mismatch remains unnoticed during stable market conditions and consistent inflows but becomes apparent when investors seek to exit – or to redeem. Chart 1 illustrates this challenge: the fixed 5% quarterly liquidity limit stands in stark contrast to redemption requests that climbed to 9.5%- 14%. The chart shows that while liquidity is fixed, investor behaviour can whipsaw.

Chart 1: Steady liquidity v unsteady redemption request

How private credit grew so quickly

To understand why this mismatch matters, it helps to look at how private credit reached this point. A decade ago, it was a niche market, largely confined to mid-market lending. But the post-2008 regulatory environment pushed banks out of riskier corporate lending, leaving a vacuum that private-credit managers were quick to fill. At the same time, years of near-zero interest rates sent investors searching for yield wherever they could find it. Private credit offered exactly what they wanted: higher returns, floating-rate protection, along with the reassuring narrative of “senior secured” lending. Plus, they were not on the balance sheet.

As the industry expanded, its investor base diversified. While pension funds and insurers were early participants, growth accelerated when asset managers introduced semi-liquid vehicles targeting high-net-worth individuals. These asset holders tend to be more responsive to news, more reactive to market mood, and quicker to redeem during phases of uncertainty. The $20 billion redemption wave marked the first time this new investor segment has reacted in the same way. All trying the exit positions or acquiring capital at the same time is eerily reminiscent of the global financial crisis of 2008 /9.

Private credit’s growth in context

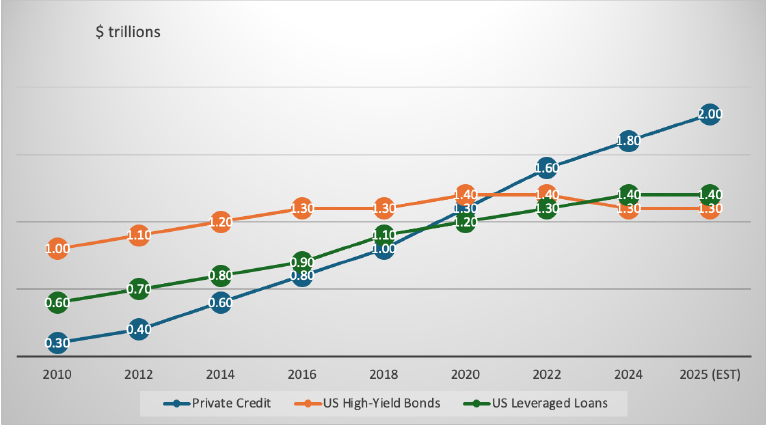

One of the most striking features of private credit’s rise is how quickly it has overtaken other parts of the credit market. A decade ago, private credit was smaller than the US high-yield bond market and far smaller than the leveraged-loan market. Today, the picture looks very different. Chart 2 illustrates this transformation. Private credit has expanded from approximately $300 billion in 2010 to nearly $2 trillion today, surpassing the high-yield bond market and the US leveraged loan market. Formerly considered an alternative financing source, private credit is now the primary channel for mid-market borrowers and is increasingly used by larger companies that previously depended on syndicated loans.

Chart 2: private credit now surpasses the USD leveraged loan market in size

This growth is worth noting because it alters the asset class’s risk profile. When private credit was relatively small, liquidity stress was a localised concern. Now, as private credit rival’s traditional public markets in scale, redemption shocks have wider implications. The industry is influencing the overall flow of credit within the economy. Consequently, private credit has evolved from an alternative asset class to a central component of the credit market.

But the redemption surge matters

Private-credit funds typically offer quarterly liquidity, but with strict caps — usually around 5% of net asset value. These limits exist because the underlying loans are illiquid: they cannot be sold quickly without discounts. In Q1, redemption requests exceeded these limits by a wide margin. Several funds received requests for 11–14% of NAV. Barings Private Credit Corp., for example, received redemption requests for 11.3% of shares but could only honour 5%. Ares and Cliffwater faced similar pressures. This forced funds to impose gates or prorate withdrawals, slowing redemptions to avoid selling assets at distressed prices. However, while this protects the portfolio, it frustrates investors who expect a smoother access to their capital.

In response to the surge, many managers moved quickly to reassure institutional clients and reinforce confidence in their vehicles. Several funds launched direct communication campaigns to update investors on portfolio health and liquidity, providing transparency into their redemption queues and asset coverage. Some firms also revisited their portfolio composition, rebalancing holdings toward more liquid assets where possible and reviewing their most vulnerable credit exposures to market stress. In certain cases, managers enhanced internal risk oversight frameworks and clarified liquidity procedures to adjust to this new environment.

Together, these steps aimed to reinforce discipline, manage redemptions in an orderly fashion, and signal to investors that the challenges were being addressed in real time. However, this mini crisis has highlighted a fundamental issue: private credit presents give an illusion of liquidity that dissipates when investors seek simultaneous redemptions.

This is not 2008, but it rhymes

It is important to be clear that this episode is not a replay of the 2008–09 financial crisis. Private-credit funds do not rely on synthetic leverage, complex derivatives, or opaque off-balance-sheet structures. They hold direct loans to companies, not CDO-squareds or synthetic tranches. The risk sits with private investors, not the banking system (though some may in fact be bank entities).

Nonetheless, there are notable parallels with 2008, particularly regarding the illusion of liquidity. Prior to the financial crisis, investors assumed mortgage-backed securities were liquid, only to discover they were not. Similarly, in private credit, quarterly liquidity was considered dependable until widespread redemption requests emerged. In both cases, liquidity breaks down gradually, then accelerates rapidly.

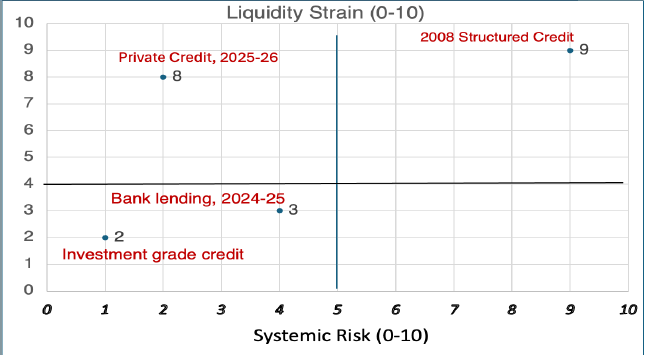

Chart 3: Private credit not as risky as 2008 structured credit products

This distinction is captured in Chart 3, which places private credit in the quadrant of high liquidity strain but low systemic risk. The stress is real, but it is contained to the sector. In short, the wider financial system is not in danger. Banks are not the transmission channel. There is no domino effect waiting to topple global markets. For context, private credit’s risk profile sits between traditional leveraged loans and high-yield bonds. Like high-yield bonds, private credit funds lend to borrowers with higher risk profiles, but the loans are typically more customised and carry fewer market protections than public high-yield bonds.

Compared to leveraged loans, private credit instruments are less liquid and often have looser covenants, but they tend to be senior in the capital structure and are directly negotiated. As a result, while private credit is less exposed to the kind of widespread contagion risk seen in public markets, it faces heightened liquidity strains and idiosyncratic risks in large-scale redemptions. Instead, the pressure is internal: funds managing redemptions, investors recalibrating expectations, and managers managing a more difficult credit environment.

Deep vulnerabilities: borrowers, leverage, and valuations

The liquidity mismatch is the most visible risk, but the deeper vulnerabilities lie in the composition of borrowers and the structure of the loans. Over the past few years, private-credit funds have increasingly lent to highly leveraged, private-equity-owned companies. Many of these firms rely on aggressive EBITDA adjustments and function with limited covenants. They are concentrated in sectors now showing indications of strain — software, healthcare services, and consumer-facing businesses.

If defaults rise, lenders may find themselves owning companies through restructurings, not because they sought equity exposure but because they inherited it. Valuations may likewise lag reality, as private loans are not marked to market like public securities. Losses can be delayed, then arrive abruptly. In response, some industry participants are moving to improve disclosure and adopt more robust valuation methods.

Several managers have enhanced portfolio disclosures or provided more frequent updates on valuation methodologies. While comprehensive mark-to-market adoption remains limited, these incremental steps reflect rising investor pressure for insight and a recognition that valuation risk is a central concern for institutional capital.

What Happens Next

The outlook for private credit depends on three forces: redemption momentum, default rates, and fundraising conditions. If investors continue to pull money out, funds may eventually need to sell loans, which could depress valuations and trigger further withdrawals. If defaults rise, net asset values (NAVs) will fall, and the feedback loop could intensify. And if fundraising slows, managers lose the ability to refinance existing borrowers, tightening credit conditions for leveraged companies.

Considering the current evolving risks, institutional investors are likely to revisit their allocation frameworks and fund management practices. Some may consider reducing their overall exposure to semi-liquid or open-ended private credit vehicles in favour of more traditional, closed-end structures with clearer exit timelines. Others might diversify liquidity sources across asset classes, increase scrutiny of redemption terms, or favour managers with demonstrated experience navigating stressed periods.

Heightened monitoring of inflows and outflows, stress-testing of portfolios under diEerent redemption scenarios, and a more conservative approach to leverage could all become more prominent in allocation decisions. For many, balancing the appeal of private credit’s higher yields against heightened liquidity and valuation risks will require more rigorous testing of portfolio construction going forward.

A crisis but not the end of private credit

The most probable scenario is a gradual tightening rather than a collapse. Private credit is expected to continue expanding, but the period of effortless inflows has ended. The industry is transitioning into a more disciplined phase, where liquid asset management, credit selection, and transparency are increasingly critical. Private credit remains a powerful and durable asset class. It fills a financing gap left by banks, offers investors attractive returns, and provides borrowers with flexibility. But the $20 billion redemption last week is a ‘shot across the bows’: the private credit model is being stress tested by the current challenging circumstances.