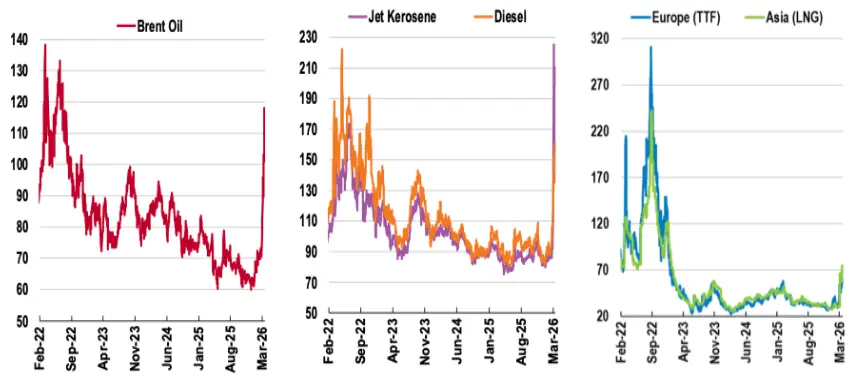

The escalation of the conflict in the Middle East has caused considerable disruption to global oil and gas markets. Between 28 February, when the war began, and 18 March, wholesale gas prices increased by 67% and oil prices by 35%. The situation has since worsened.

As of 19 March, Brent crude reached $114–$115 per barrel, marking its highest level since the conflict escalated, following a 7% overnight increase. UK natural gas futures rose to approximately 170-174p per therm, representing a 25% increase in a single day and a 40% rise over the past week, following attacks on Qatar’s LNG export hub in response to Israeli strikes on Iran’s South Pars gas refinery.

Chart 1. Global Energy prices have spiked

These sharp movements have inevitably led to comparisons with the spike in energy prices following the outbreak of the Russia–Ukraine war in February 2022 and calls for the government to provide relief for households and businesses. The earlier crisis prompted a massive fiscal response in the UK, costing around £75 billion over two years – almost 3 per cent of GDP – and far larger than the support packages deployed in most European countries. Already, there are demands to help households reliant on heating oil and to extend the temporary 5p cut in fuel duty introduced in 2022.

Several European countries are implementing targeted measures in response to the renewed energy shock. Germany has announced a temporary reduction in VAT on energy bills and is considering additional support for vulnerable households. France has maintained a cap on electricity price increases at 10 per cent and is providing direct rebates to lower‑income families. Italy has extended tax credits on energy costs for firms most exposed to price increases and continues to subsidise domestic consumers. Spain has prolonged fuel subsidies and temporarily reduced energy taxes.

These diverse policy responses offer benchmarks for the United Kingdom to pursue, illustrating alternative strategies to protect households and businesses from energy market volatility while balancing fiscal sustainability with targeted relief.

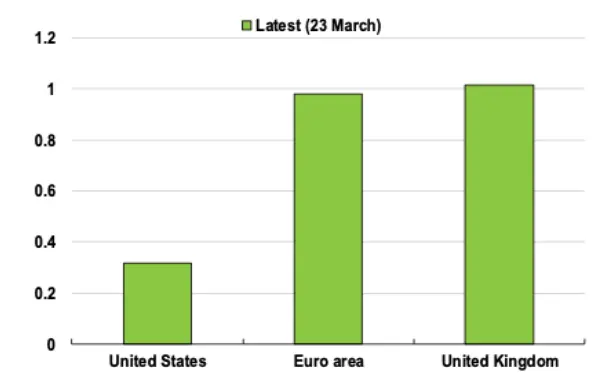

But a key question is whether this new shock will produce inflationary and macroeconomic consequences comparable to those of 2022, and what implications it holds for the Bank of England’s interest‑rate decisions. At its March meeting, the Bank maintained rates, noting that “the MPC is alert to the increased risk of domestic inflationary pressures through second‑round effects in wage and price‑setting, the risk of which will be greater the longer higher energy prices persist. The MPC is also assessing the implications for inflation of the weakening in economic activity that is likely to result from higher energy costs.” See chart 2 for market views.

Chart 2. Market based 2-year inflation expectations

Increase since 27 February, percentage points

A Smaller but still significant shock

To date, the increase in wholesale gas prices, while substantial, remains well below the scale observed in 2022. Between 2021 and late 2022, gas prices tripled in real terms, while oil prices rose by 27 per cent before subsequently declining. The current price increases, though pronounced, are smaller and start from a lower base.

Presently, household energy bills are 14 per cent higher in real terms than before the Ukraine war; however, the Ofgem price cap for April (£1,641) is significantly below the real‑terms level that triggered government intervention in 2022–23 (£2,699). Only if current wholesale price increases are sustained and are fully passed through would bills slightly exceed that threshold.

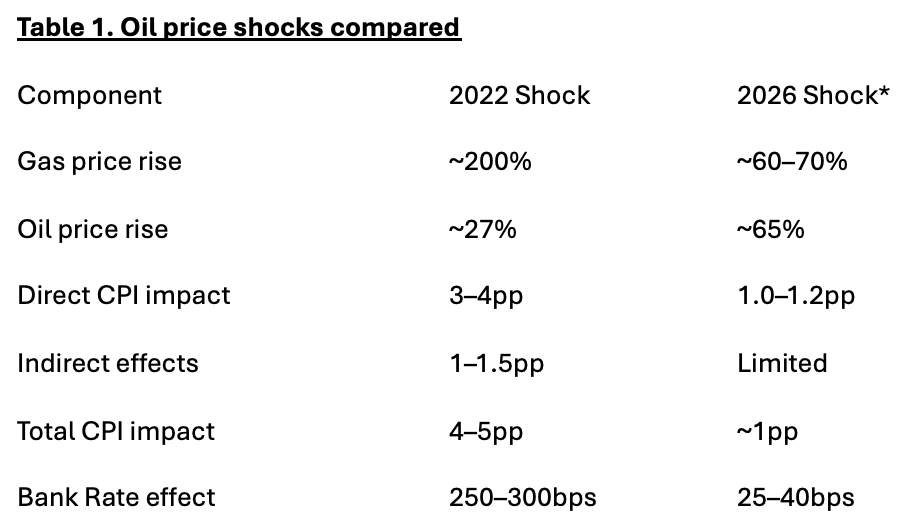

This distinction is significant for inflation dynamics. In 2022, the surge in wholesale gas prices was directly reflected in the price cap, driving annual CPI inflation above 11 per cent and prompting rapid monetary policy tightening. Currently, the pass‑through is expected to be smaller and slower, mitigated by the cap resetting to a lower level (see Table 1).

A stylised model of the inflation impact

To assess the likely inflationary consequences of the current shock, a simple model based on standard macroeconomic relationships or elasticities is instructive. A sustained 10 per cent increase in oil prices typically contributes approximately 0.05–0.07 percentage points (pp) to CPI inflation. With oil prices currently up about 65 per cent month‑on‑month, the implied CPI effect is roughly 0.3–0.4pp. The pass‑through from gas is larger: a 100 per cent increase in wholesale gas prices adds approximately 1.0–1.2pp to CPI over a year. With gas prices up 60–70 per cent over the past month, the implied CPI effect is around 0.7–0.8pp.

In total, the current shock is estimated to add approximately 1.0–1.2pp to CPI inflation. This impact will mean it will miss the inflation target for at least a year, potentially stymying any rate cut, but it is still considerably smaller than the 2022 episode; see Table 1. Table 2 shows a more pessimistic scenario. Meanwhile, chart 3 shows the total impact for the UK compared with the other OECD countries.

Chart 3: Inflation is some 1% higher for many countries

Implications for Bank Rate and Rationale for the March Decision

While the Bank of England does not adhere to any mechanical formula for determining interest rates, the ‘Taylor Rule’ offers a useful framework. In its simplest form, the rule suggests that for every 1 percentage point increase in inflation above target, interest rates should rise by more than 1 percentage point in the long run (technical note available on request). However, central banks typically smooth their responses over time.

Applying a smoothed Taylor Rule framework to the current shock indicates a modest upward adjustment in the Bank Rate trajectory – approximately 25-40 basis points, or more plausibly, a delay in the timing of the first rate cut. This adjustment is substantially smaller than the 250–300 basis points of tightening associated with the Ukraine shock.

This rationale underpins the Bank’s decision to maintain rates in March. However, the Committee recognised the increase in energy prices but determined it was insufficient to reverse the broader disinflationary trend. Wage growth is moderating, services inflation is gradually declining, and inflation expectations remain stable. The Bank’s communication emphasised vigilance but indicated that while the shock is significant, it does not warrant a return to aggressive tightening.

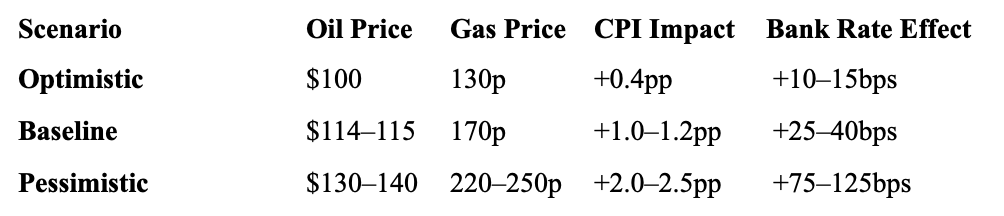

However, that is only if the situation does not get considerably worse. In the scenario below, we suggest it could trigger a rate rise if the sustained increase in oil prices above $130 a barrel is matched by a rise in gas prices to 220–250 pence per therm. In that scenario, annual CPI inflation could jump another 2 to 2 1/2 percentage points, taking the headline annual rate to 6-7%.

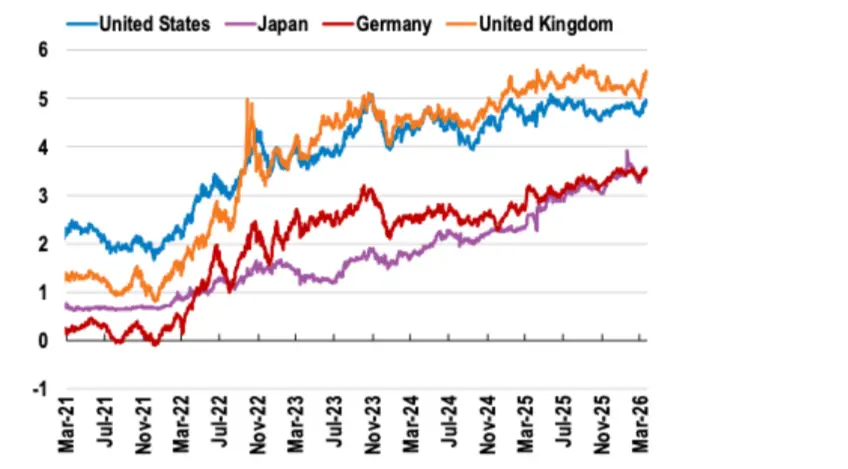

Furthermore, financial market interest rates currently reflect a more concerning long-term debt outlook for the United Kingdom compared to other G4 economies (see chart 4). Annual UK debt interest payments exceed £100 billion and, according to the Office for Budget Responsibility (OBR), are projected to increase by an additional £47 billion by the end of the current parliament in 2031. This increase would position debt interest payments as the third largest component of UK public expenditure, surpassing spending on education and defence, with only social security and health budgets remaining higher.

Chart 4. The rise in inflation expectations is already raising UK long term interest rates, to the highest among the G7 economies

Table 2. Worst-case assumptions

Fiscal policy is less flexible today than in 2022

Even with a smaller inflationary impact, the fiscal consequences of a sustained increase in energy prices could be substantial. The Office for Budget Responsibility (OBR) estimates that a 75 per cent rise in oil and gas prices sustained for one year would increase public sector debt by 3 per cent of GDP after three years, primarily due to higher welfare spending and debt‑interest costs.

Maintaining departmental budgets in real terms (that is, adjusted for price inflation) would add 2 per cent of GDP. Since UK borrowing costs are now significantly higher than in 2022, making large‑scale support packages are much more expensive to finance.

This context underscores the importance of carefully targeted fiscal relief. Universal measures, such as broad‑based price caps or fuel duty reductions, are straightforward to implement but can be costly and less efficient, often benefiting higher‑income households alongside those most in need.

Alternatively, targeted interventions – such as direct payments to vulnerable households, means‑tested rebates, or time‑limited tax credits -can provide effective support while containing overall fiscal costs. Each approach involves trade‑offs around speed, administrative complexity, and the precision of support delivery, making the design of future interventions a critical policy consideration.

Windfall taxes implemented in 2022 have generated approximately £15 billion; however, the government is already dependent on this revenue stream. Replicating the scale of the 2022 support package would require additional tax increases or new measures, both of which pose significant political and economic challenges. Alternative revenue options include expanding windfall taxes to additional sectors that have benefited from recent financial market volatility, introducing temporary levies on high‑income individuals, or reducing costly tax exemptions.

Additionally, efficiency savings across government departments and enhanced efforts to address tax avoidance could help offset the fiscal burden. None of these options are palatable after around £80bn of tax rises since the current administration took office.

This fiscal shock Is smaller, for now

The current energy shock is substantial and politically significant, but it does not – yet – mirror the scale of 2022. The inflationary impact is expected to be approximately one percentage point, rather than five. The Bank of England’s decision to maintain rates in March reflects this assessment: while the shock may delay the timing of rate reductions, it does not imply a new tightening cycle – the economy is too weak, and the inflation impact of this crisis is much smaller. The fiscal response also weakened – it is about designing efficient, targeted support rather than mobilising tens of billions of pounds the government does not have.

Targeted support could include means‑tested subsidies for low‑income households, direct rebates for vulnerable groups such as pensioners or individuals with disabilities, and time‑limited energy vouchers for those most affected by higher bills. Additional measures might involve expanding eligibility for existing welfare payments or providing tax credits for firms facing extreme input‑cost pressures. These approaches will concentrate resources where they are most needed and minimise costs.

In summary, while this shock is extremely unwelcome – particularly as recent data indicate slowing UK wage growth while the unemployment rate is stuck at 5.2 per cent, though with an upward bias – it remains less severe than the situation four years ago following Russia’s invasion of Ukraine. However, events are unfolding rapidly, and it is not yet clear how they will end, adding to uncertainty and harming UK economic activity, business investment, and hiring decisions.