LMA News – 20th Anniversary Edition

Overview

In the last 20 years, the world economy has continued to evolve at a fast pace, perhaps faster than ever. It has always changed, but a quicker pace of technological innovation, across a broader range of areas and involving a greater number of people in more countries than ever before, means that the pace is accelerating. Although the first industrial revolution started in the UK and Europe in the 1750s, it has now spread around the world, and the current advances involve 7 bn people participating in the same global economy, using the same rules and market-based system to generate wealth and raise living standards.

That necessarily increases the speed, adoption and spread of change by multiples compared with the past. This is partly due to the power of compounding: doubling something that is getting bigger means it gets bigger even faster. If a country’s economy grows by 7% for ten years, its GDP will double. When measuring economies globally, the International Monetary Fund (IMF) uses something called Purchasing Power Parity. Effectively, it translates each country’s GDP using a calculation, which adjusts for differences in spending power between countries. For instance, a haircut in China will be cheaper than a haircut in the US, meaning that an equivalent dollar will buy you more resources in the poorer country than the richer one.

To many, the fast pace of change is unsettling. In economic terms, what is required is that the winners of these developments compensate the losers, rather than losers continuing their efforts – doomed to fail – to stop progress. As any review of global economic history shows, economic development is something that cannot be halted, and even disruptive events such as war or recession have temporary, not permanent, effects. A country that tries to duck change usually ends up getting left behind.

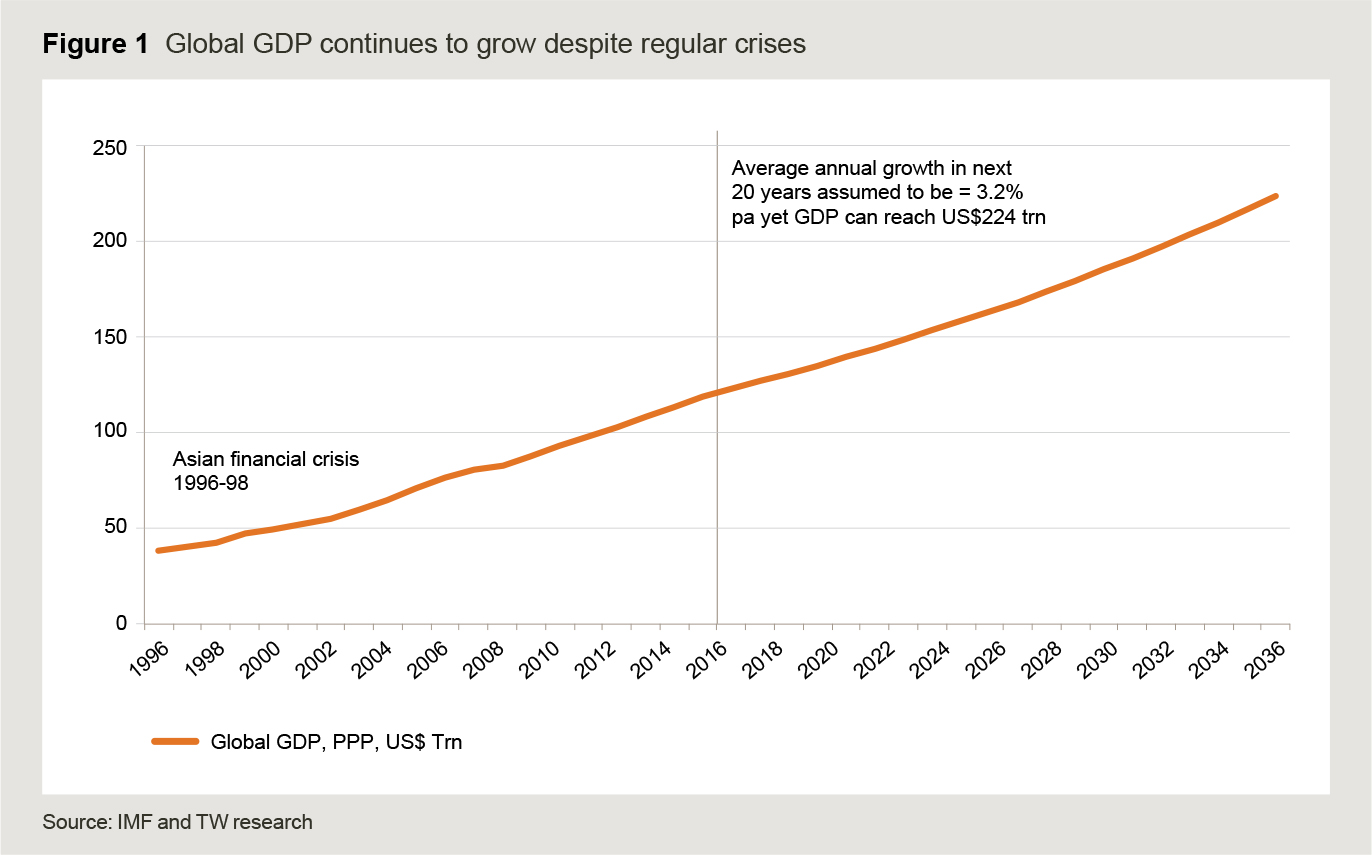

Figure 1 shows how strong global GDP growth has been in the last 20 years, despite the periodic crises that it has experienced. Global GDP passed the US$100 trn mark in PPP terms in 2013, expanding by 2.6 times its 1996 value. Even assuming that GDP grows at half the pace of the period between 1996 and 2016 – that is to say at 3% a year rather than 6% – global GDP in PPP terms will surpass US$200 trn in 2033. Of course, this assumes that the acceptance of the market economy remains globally intact.

The pace of growth in the last 20 years proves the continuing ability of the world economy to generate wealth. Despite the biggest economic recession since the great depression of 1929, and the global Financial Crisis, the world economy has continued to expand. In 1996, China’s economy was just 30% of the size of the US. By 2015, it was bigger in PPP terms, having expanded 8 times, compared with 2.2 times for the US economy.

Notwithstanding the challenges, more people than ever before can afford more goods and services. There are fewer poor – some 40% less over the last 20 years – and more people on middle and lower middle-incomes. The latter can now afford products and services that in previous epochs would have only been available to, and exclusively for, a narrow elite. That is why economic growth has been so much faster; more people have moved into the bracket that drives an economy faster than ever before. The number of individuals in the middle-income segment has grown from 1.9 bn people in 1996 to 3.2 bn in 2016, according to data from the Organisation for Economic Co-operation and Development (OECD).

With the global population heading towards 9 bn in 20 years’ time – mainly down to faster population growth in poorer countries – the likelihood is that global GDP growth will also accelerate. This is because economic growth is the sum of productivity (of labour, capital and innovation) and increase in labour force. Assuming that productivity equalises around the world – as it seems to be doing, as everyone adopts the market economy – then countries with a faster growth in population will tend to have faster economic growth.

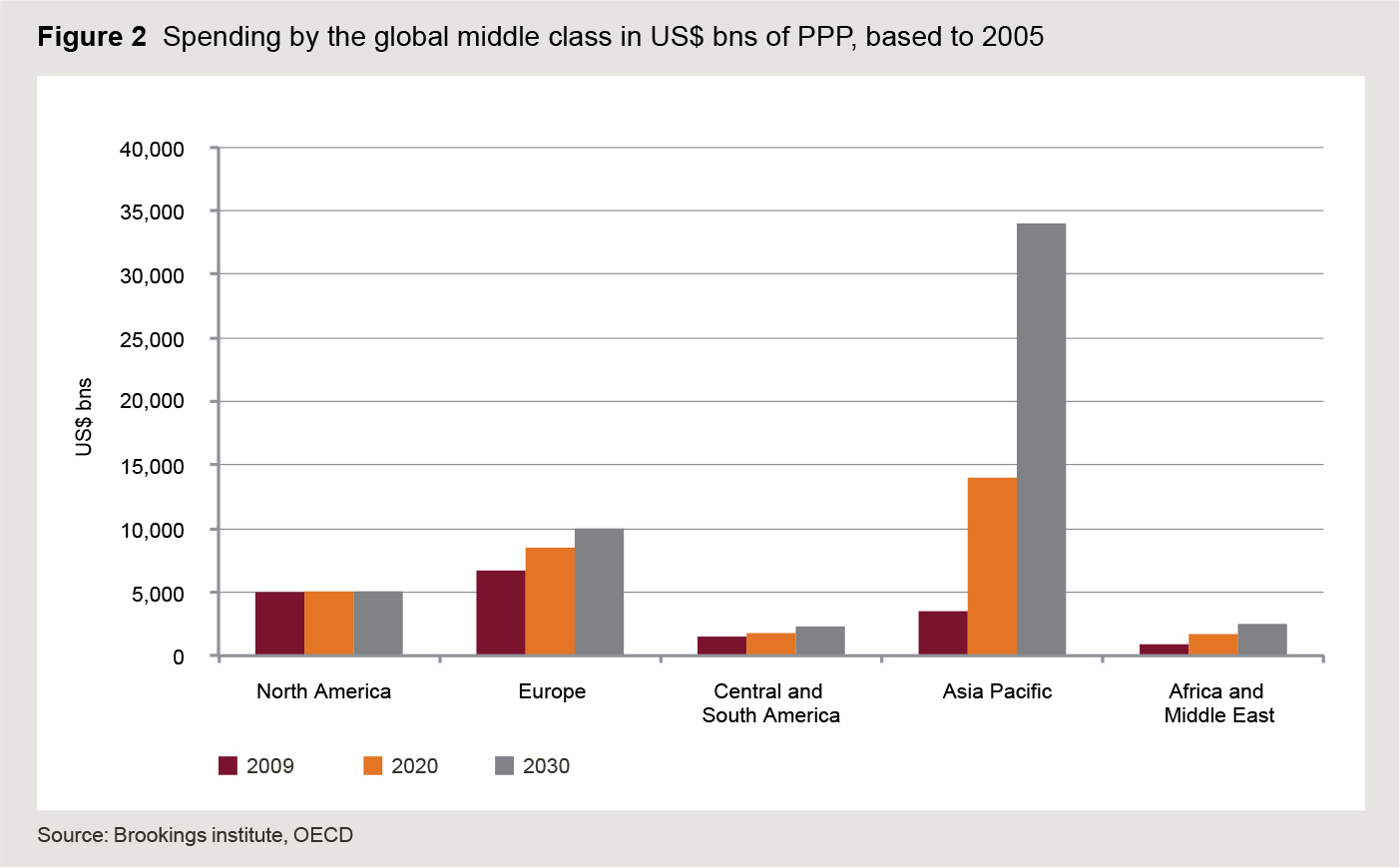

What this means regarding shares of global spending is shown in Figure 2. It will be dominated by Asia, where population expansion, a growing middle class and high productivity is generating the biggest number of people with high spending power than anywhere else. Even by 2020, the region will have the largest share of global spending, measured on the vertical axis. By 2030, its share will have more than doubled.

What this means regarding shares of global spending is shown in Figure 2. It will be dominated by Asia, where population expansion, a growing middle class and high productivity is generating the biggest number of people with high spending power than anywhere else. Even by 2020, the region will have the largest share of global spending, measured on the vertical axis. By 2030, its share will have more than doubled.

Challenges remain, and crises are always with us

A possible point of inflexion or turning point for regional shares of total global growth seems to have been reached. Emerging economies now account for a larger proportion of GDP than advanced economies. This is the first time this has occurred since the industrial revolution ratcheted up growth in Europe in the 18th century. This turning point is altering global power relationships between countries and, allied with the communications revolution, a more integrated world has to deal with the challenges this throws up.

Nowhere has this been more evident than in some of the events of the last 20 years. We have seen the advent of the euro in 2000, the great recession and the global financial crisis, Brexit fears and now Brexit. One can and should also include the wars in Libya, Iraq, Syria, and the Yemen. There was a popular uprising in Egypt, which overthrew dictators that had been in power for over 30 years, only for the government that took over from them to be overthrown in turn by the former military rulers.

In Europe, we have had wars in Georgia, Crimea, Ukraine, and now Syria. Despite this, the news is not all bleak: global poverty has fallen, and global wealth has increased.

What about the future economic impact of Brexit on the UK?

In the long run, no one can say for sure that they know what the economic implications of the UK’s exit from the EU will be. Much of that depends on what sort of deal is struck and how the UK responds to its “independence” to chart its course in the world, free from cooperating with 27 other countries in the EU.

For instance, if the UK forges a deal similar to Norway, which is allowed access to the EU market but must accept free movement of people and pay an entry fee, perhaps the impact would not be that significant. But if, as it seems, free flow of individuals were anathema to many who voted to leave, this approach would be a non-starter.

If, on the other hand, the UK could create a deal similar to the recent one concluded between the EU and Canada, which focused on trade but had no free movement of people, this might be acceptable to the camp amongst leave voters who want to reduce immigration drastically. That deal, however, still took nearly 8 years to conclude and will not be as beneficial as the deal the UK has as a full member of the EU.

Indeed, it appears that the UK will first have to negotiate its way out of the EU, which could take two years and then negotiate a new trade deal, which could take a further 3 to 10 years (if we base this on the EU’s speed of negotiation with other countries). In the longer run, what happens will rest on the deal struck with the EU and the success of the UK in forging new ties with the remainder of the world to replace its EU links.

There are two useful economic nostrums to bear in mind when thinking about the benefits of the size of markets and trading, though. First, we must remember that nearly 200 years ago, David Ricardo, a British political economist, proved freer trade benefits all countries, even if one of them lowered barriers unilaterally. Indeed, even if, in absolute terms, one country produced everything more cheaply, it will still prove worthwhile to trade as, in relative terms, they will not produce everything better. No country produces everything relatively better than every other country, so producing what you are best at means cheaper goods and higher living standards. Second, the fact is that a bigger market offers greater economies of scale, lower average costs and higher profitability. This means lower prices for consumers, leaving them with enough remaining spending power to buy other goods and services, and so boost economic activity.

From a macroeconomic perspective, these outcomes result in increased investment spending and this, in turn, generates higher levels of productivity. This process leads to higher paid jobs, greater levels of employment and raised living standards. A smaller economy with fewer trading links and slower growth in the labour force inevitably results in slower economic growth than in a bigger economic zone. For this reason, multilateral deals are always better than bilateral deals.

What to look for in the next 20 years

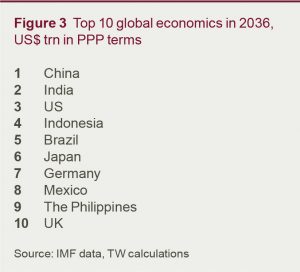

What about future GDP growth? That will be driven by changes in productivity and population. I have used this approach to calculate the top ten global economies in 2036, shown in Figure 3. Using the IMF measure from 2015 of the top ten based on PPP gross domestic output, out go Russia, France and Italy and in come the Philippines, Mexico and Brazil in 2036.

Interest rates are still at record lows, and return to pre-financial crisis levels is not on the cards for the next two decades. Interest rates, however, are rising in the US at the moment, and an increase in the UK and euro area is possible in the next five years, but highly doubtful in Japan in the next ten years.

Major challenges seem to come from economic, social, and political feedback loops. The next few years will be dominated by a political effort to make sure that those who feel left out and excluded from the economy are brought into the fold. The sort of action required to do this is not difficult to figure out. We need better schooling for the rural and urban poor so that they can get the jobs of tomorrow rather than the jobs of yesterday. We need social housing, not just affordable housing – which is often still far too expensive – but housing backed by local authorities with public money so that communities are strengthened rather than broken. We need more technical colleges and vocational training. There needs to be devolution of power from central governments so that local politicians can take decisions about the issues such as schooling and housing that affect their communities.

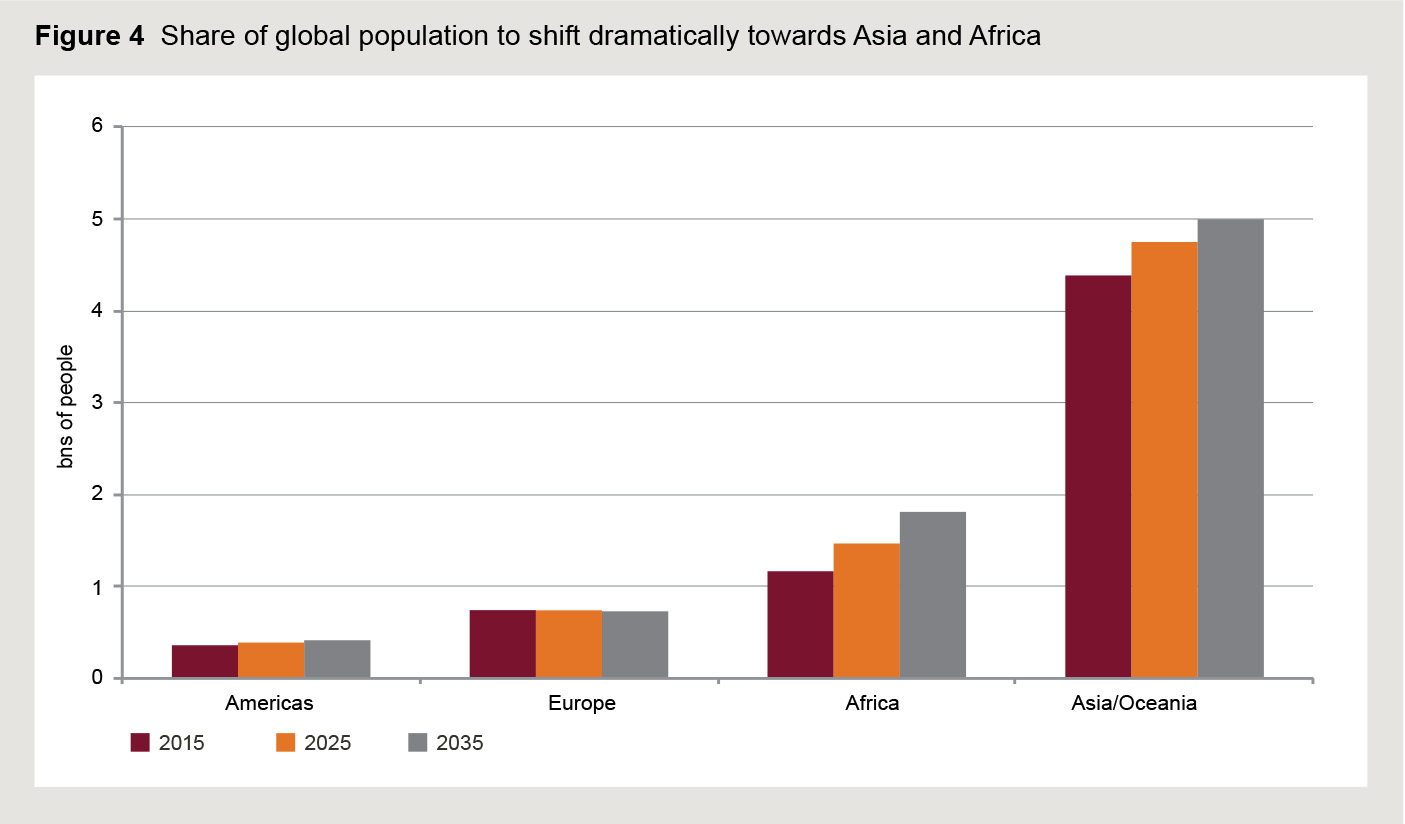

Global population continues to increase. Figure 4 shows that Asia, driven by Chinese and Indian population increases, will grow its share, along with Africa. This will have a profound impact on the distribution of global GDP in the next 20 years. United Nations projections suggest that the world’s population will reach 8.7 bn by 2036, from 7.2 bn last year. Although the number of people from Asia will rise to 5 bn, their share of the total will fall, as African population growth is even faster. Europe’s population will peak at about 730 mn, and the US will rise towards 415 mn from the current 360 mn. Cities – ever the most important for growth – will remain the key drivers of economic activity and growth within countries.

Global population continues to increase. Figure 4 shows that Asia, driven by Chinese and Indian population increases, will grow its share, along with Africa. This will have a profound impact on the distribution of global GDP in the next 20 years. United Nations projections suggest that the world’s population will reach 8.7 bn by 2036, from 7.2 bn last year. Although the number of people from Asia will rise to 5 bn, their share of the total will fall, as African population growth is even faster. Europe’s population will peak at about 730 mn, and the US will rise towards 415 mn from the current 360 mn. Cities – ever the most important for growth – will remain the key drivers of economic activity and growth within countries.

The rapid pace of technological change will persist, becoming an enabler across a range of industries rather than a separate business sector. Interest rates will rise in the US towards 3-4%, in line with nominal GDP, which will likely consist of 2% inflation and 2% real growth (despite efforts from US President-elect Trump to get growth up to 3-4% per annum). For the UK, interest rates are likely to rise, but by much less than in the US, as low UK productivity gains keep growth subdued. Japanese interest rates may remain close to zero, although increase from the current negative territory. Anaemic growth of 1%, allied with inflation at zero, will keep interest rates low.

As for currencies, the US dollar should remain solid against the yen, euro and sterling, but the latter will continue to be weak versus the euro.

The avoidance of conflict will be essential, particularly between the US and China. Wars will become less frequent – difficult though that may be to believe – as they have done since World War Two. Democracy has spread, and will continue to spread, around the world alongside promises of faster economic growth.

Unfortunately, this does not mean wars will end. Eastern Europe could remain an area of instability if Russia’s economy suffers from a lack of investment and growth as many suspect it will. Africa remains a significant opportunity, but the population dividend (growth in the working-age population relative to the elderly) has to be harnessed by greater economic efficiency and policies to promote human capital growth. If not, the big population increases estimated in this article will breed instability and poverty in countries like Ethiopia and Nigeria, rather than create greater wealth.

Western Europe will remain a key financial and economic powerhouse for the next 20 years but faces a lower share of global GDP, as its population declines in absolute terms and as a share of the global total. Challenges persist in democratic legitimacy and changes in the membership of the euro area are not inconceivable, with new members perhaps joining, but others leaving.

Conclusion

In the next two decades, one thing is for sure: there will be profound change. Demographic shifts mean that the European share of the world total population will slip to about 7%, and Asia’s share will rise towards 60%, as Africa and the Middle East pick up to around 25%. Economic shares will increasingly reflect this trend, and the world will become more multipolar, as the economic and political dominance of the US continues to slip.

The world, however, is likely to become more economically integrated, as globalisation, international trade, and communications technology remain vital forces binding it closer together. However, the political risks of this greater integration could rise, if those who feel excluded are not included in the benefits of rising wealth. It is impossible to know the precise timing or cause of future economic, and banking shocks (they shall remain known unknowns), but it is almost assured that they will happen – just as they have in the last 20 years.

What is also likely, though, is that the continued upward march of global living standards will also persist. If there is one lesson from the last 20 years, it is that nothing – not even the worst economic slowdown in 100 years – can stop the advance of global economic prosperity, as the market economy spreads to include the entire world and the pace of technological change impacts more industries than ever before.